The Basic Principles Of Mortgage Lender

Federal governments normally regulate lots of facets of mortgage lending, either directly (with legal demands, for example) or indirectly (via policy of the participants or the monetary markets, such as the financial sector), and also typically with state intervention (direct loaning by the federal government, direct lending by state-owned financial institutions, or sponsorship of numerous entities) - Home Equity Loans.

Mortgage are usually structured as lasting loans, the routine settlements for which are similar to an annuity and also determined according to the time value of cash solutions - Mortgage Lender. One of the most fundamental plan would call for a dealt with monthly payment over a period of 10 to thirty years, relying on local conditions.

Home mortgage lending will certainly also take into consideration the (perceived) riskiness of the home mortgage car loan, that is, the chance that the funds will be repaid (typically considered a feature of the credit reliability of the debtor); that if they are not settled, the lender will certainly be able to confiscate on the realty assets; and the financial, rate of interest danger as well as dead time that might be associated with certain situations - Mortgage.

Current Mortgage Rates for Dummies

There are numerous kinds of mortgages used worldwide, yet a number of variables broadly specify the attributes of the home loan. All of these may go through neighborhood regulation as well as lawful requirements. Interest: Interest may be dealt with for the life of the finance or variable, and also modification at certain pre-defined periods; the interest price can likewise, naturally, be greater or reduced.

The two fundamental types of amortized finances are the fixed price mortgage (FRM) as well as adjustable-rate home loan (ARM) (likewise referred to as a floating price or variable rate mortgage) - Mortgage Lender. In some nations, such as the USA, repaired rate home loans are the standard, however floating rate home loans are reasonably typical. Combinations of taken care of as well as floating price mortgages are also typical, where a mortgage will have a fixed price for some duration, as an example the very first five years, and differ after the end of that duration.

When it comes to an annuity repayment scheme, the regular settlement continues to be the exact same quantity throughout the lending. When it comes to linear repayment, the periodic repayment will slowly lower. In a variable-rate mortgage, the rates of interest is usually taken care of for an amount of time, after which it will regularly (for the original source instance, annually or monthly) adjust up or down to some market index.

Considering that the threat is transferred to the borrower, the first rates of interest might be, for example, 0.5% to 2% less than the typical 30-year fixed rate; the size of the rate differential will certainly be associated to financial debt market conditions, consisting of the yield curve. The charge to the consumer depends upon the credit score risk in addition to the rates of interest danger.

Not known Details About Interest Rates

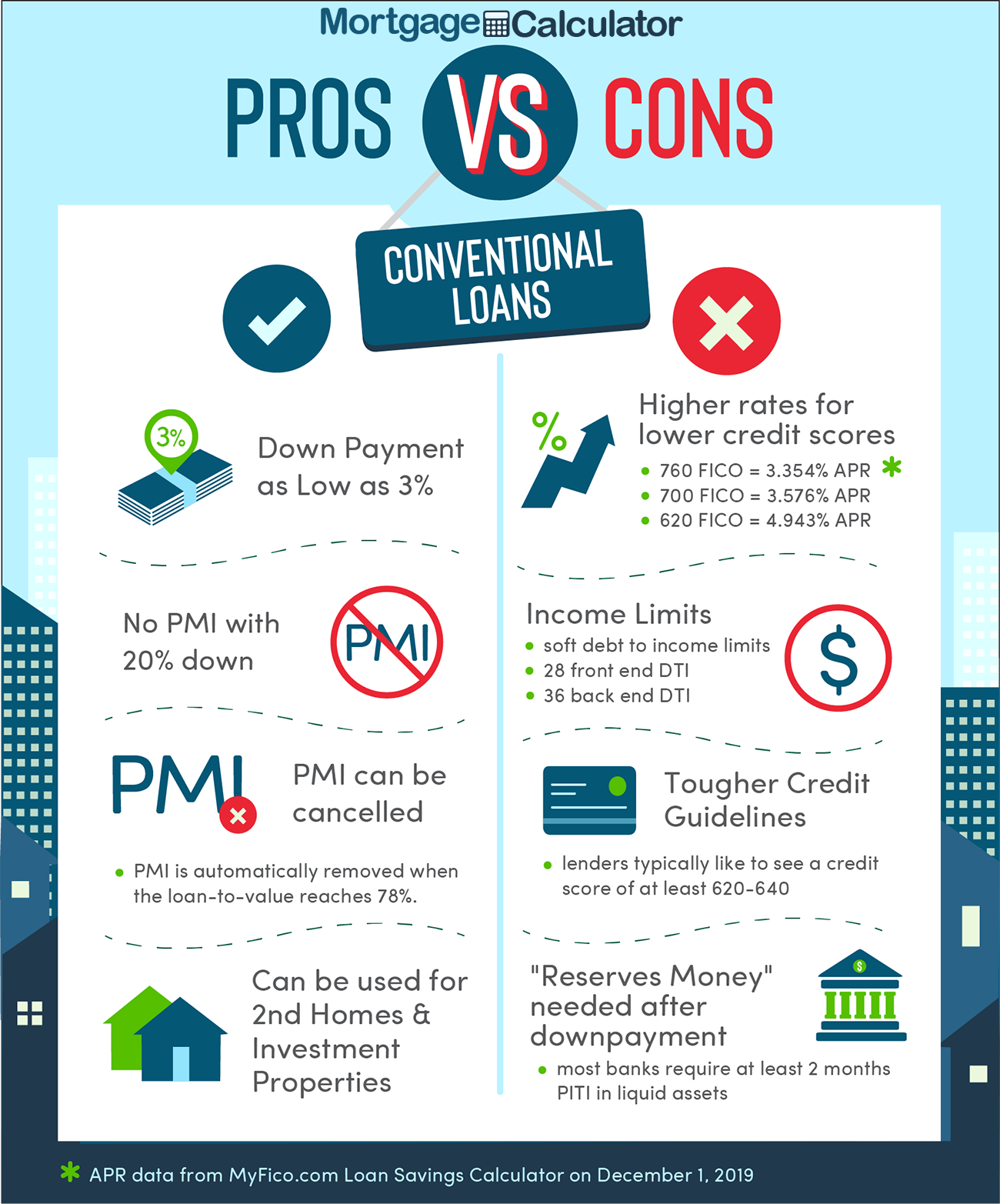

Big home mortgages as well as subprime borrowing are not supported by government guarantees and also deal with greater interest rates. Various other advancements Read Full Report described below can influence the prices as well. Upon making a home mortgage financing for the purchase of a residential property, loan providers usually call for that the consumer make a deposit; that is, add a part of the cost of the residential or commercial property.

The car loan read what he said to value proportion (or LTV) is the size of the funding versus the worth of the building. Consequently, a mortgage in which the buyer has made a down repayment of 20% has a loan to value ratio of 80%. For fundings made against homes that the debtor currently owns, the loan to worth ratio will certainly be imputed versus the approximated value of the residential property.

Because the value of the property is an essential consider understanding the risk of the funding, figuring out the value is a vital factor in home loan financing. The worth may be established in numerous ways, however the most common are: Real or purchase worth: this is typically required the acquisition price of the residential property.

Usual actions consist of settlement to income (home mortgage repayments as a percent of gross or internet revenue); financial debt to income (all financial debt repayments, including mortgage payments, as a percentage of income); and various web well worth actions. In lots of countries, credit report are used in lieu of or to supplement these steps.

Interest Rates Fundamentals Explained

the specifics will vary from place to place. Some lending institutions might also require a possible borrower have several months of "book possessions" offered. Simply put, the consumer may be needed to reveal the availability of adequate properties to pay for the housing prices (consisting of home mortgage, taxes, and so on) for a time period in the event of the task loss or various other loss of income.